It was just over 9 years ago today when we wrote “The Incredibly Shrinking Market Liquidity, Or The Upcoming Black Swan Of Black Swans” in which we explained how as a result of the growing influence of HFT, quants and central banks, the market itself was breaking. We also highlighted what the culmination of the market’s “breakage” could look like:

liquidity disruptions could and will lead to unexpected market aberrations, such as exorbitant bid/ask margins, inability to unwind large block positions, and last but not least, explosive volatility: in essence a recreation of the market conditions approximating the days of August 2007, and the days post the Lehman collapse…

We even laid out some possible catalysts for a possible market crash: “continued deleveraging in quant funds, significant pre-market volatility swings as quants rebalance their end of day positions, increasing program trading on decreasing relative overall trading volumes.”

We saw all of the above elements briefly come together when on February 5 the market finally did break in one spam of exploding volatility, as its topology was torn apart by various, disparate elements, resulting in virtually all of the above materializing, if only for a short time, and blowing up the VIX, which soared by the most on record, rising from the lower teens to above 50 in the span of hours, while bankrupting countless vol sellers.

Since then, the same elements that coalesced in 2017 to pressure and keep the VIX at its lowest level in history reemerged, and the “selling of volatility” once again reappeared as a dominant trading strategy, but not before Goldman Sachs wrote a report in March in which it echoed everything that we warned about over 9 years ago, and which increasingly many have said in the past decade, namely that the advent of algo trading and HFTs have collapsed market liquidity to the point where the market itself has become precariously brittle, prompting increasingly frequent flash crashes, and leading Goldman to conclude that, when it comes to market risk factors, “liquidity is the new leverage” in a world in which HFTs are the marginal price setters:

One conspicuous consequence of post-crisis evolution is that trading volumes in many markets are now dominated by high-frequency traders (HFTs). While bid-ask spreads and other indicators of trading liquidity appear to indicate liquidity has improved in markets where HFT has grown, the quality of this liquidity has not yet been stress-tested by recession. The recent experience of the “VIX spike” suggests there is good reason to worry about how well liquidity will be provided during episodes of market distress, and this is only the latest example of a “flash crash”. Regulators and researchers increasingly warn that HFT strategies can contribute to breakdowns in market quality during periods of distress.

Ominously, Goldman repeated our conclusion from 2009, almost verbatim, and said that “along with the uncomfortably high number of flash crashes in most major markets, we think “markets themselves” belong on the short list of late-cycle risks to which markets are potentially complacent.”

* * *

Fast forward to today when Goldman strategist Charles Himmelberg is back with a new report, which picks up where his last piece left off, defining “Liquidity as the New Leverage”, and asking – rhetorically – “Will Machines Amplify the Next Downturn?”

The answer, of course, is “yes” as we have warned non-stop for almost 10 years now, but it is always gratifying to hear some non-tinfoil hat-wearing Goldmanite, i.e. FDIC-insured recipient of taxpayer bailouts, confirm it and that’s just what Himmelberg has done, warning that“the rising frequency of “flash crashes” across many major markets may be an important early warning sign that something is not quite right with the current state of trading liquidity.”

For those unaware, if and when Goldman says “something is not quite right”, it’s time to quietly exit, stage left.

These warning signs plus the rapid growth of high-frequency trading (HFT) and its near-total dominance in many of the largest and most widely traded markets prompt us to more carefully consider the possibility (not necessarily the probability) that the long expansion accompanied by relatively low market volatility may have helped disguise an under-appreciated rise in “market fragility.”

To be sure, the topic of rising market fragility is anything but new to regular readers, and we have been covering it extensively over the past two years, although Goldman’s growing concern by what was painfully obvious to many traders gives hope that one day the Fed too may be able to grasp just how its actions have broken the market, although that realization will sadly take place just moments before a historic market-wide flash crash send the S&P plummeting by the most ever, resulting in a market that is indefinitely halted.

But how do we get there?

First, it is time for traders, economists and policymakers to realize that, as Goldman recently “discovered”, liquidity and not leverage, is now a systemic risk; ironically, in a world in which traders think there is copious liquidity across all asset classes, the reality is that there is virtually no true providers of liquidity when one needs it. Here is Goldman, which confirms that “Liquidity poses a potential systemic risk.”

While investors may be settling for ever smaller premia in exchange for liquidity risk, we see far less scope for systemic risks arising from the post-crisis search for yield…. by flagging the risk that a post-crisis erosion of trading liquidity may be contributing to an under-appreciated rise in “market fragility.”

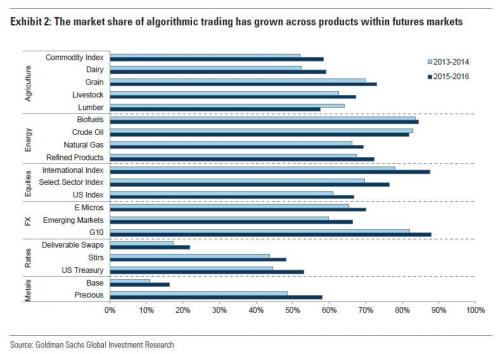

The past 10 years have seen fairly dramatic changes in the regulatory environment, industry composition, and the trading technologies by which liquidity is supplied to markets. The resulting market evolution is one in which algorithms are replacing people, and speed is replacing capital. Exhibits 1 and 2 show how the volume share of algorithmic traders has grown by asset class and across products in futures markets.

Iran Announces Plan To Stay In Syria As Pompeo Issues…

After last Thursday’s relatively brief meeting in Sochi between Russian President Vladimir Putin and Syria’s Bashar…

But why is Goldman confident that the new market structure is prone to (terminally) breaking? For the simple reason that nobody has ever tested the market’s anti-fragility, to borrow a term from Taleb, and the only way such a test can take place is during a violent market crash, one in which central banks do not step in and bail out markets. However, with central bankers all-in asset reflation, that is unlikely. Which leads us to the following point from Goldman:

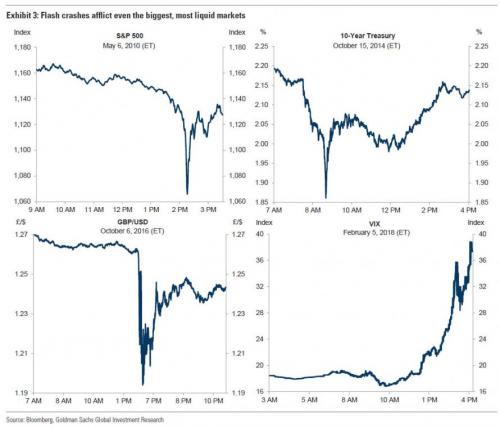

Is this new market structure more prone to market fragility? It is hard to say, since it has not yet been tested by a recession or major market correction (and this alone is a risk worth flagging). But the rising incidence of “flash crashes” provides little cause for comfort (Exhibit 3). The fact that even some of the biggest, most heavily traded markets appear vulnerable to flash crashes provides plenty of ex-ante reason to worry that these small cracksin the foundation may betray deeper structural issues that have simply not yet been exposed.

Of course, the best, most recent example of such a “small crack”, and the catalyst for Goldman’s renewed focus on this question, was the VIX spike, i.e. volocaust, on February 5, 2018, when the VIX had its largest one-day move in its history. There was nothing in the fundamental data to explain a jump of this magnitude. Instead, the VIX spike was clearly a reflection of technical trading dynamics. Goldman here notes that while a number of factors may have contributed to the surprising magnitude of this spike, most importantly the design of certain exchange-traded vol products, it was pretty clearly amplified by poor market liquidity.

While many of the causes leading to the VIX spike were unique to the VIX, our liquidity concerns are driven by developments that could be common to virtually all liquid asset markets.

At this point Goldman, which is clearly growing increasingly worried about an imminent, wholesale market collapse resulting from a break in market structure itself, lays out a grand unified theory why the post-crisis frequency of flash crashes could be symptomatic of a broader rise in “trading fragility”, and it all goes back to our old friends, the parasitic frontrunners of orderflow better known as high frequency traders or HFTs, who are there to generously provide liquidity when nobody needs it, and shut down, draining all market liquidity, every time it is needed. Goldman’s description is far more poetic:

HFTs know the price of everything and the value of nothing. One theory that has been proposed for why market fragility could be higher today is that because HFTs supply liquidity without taking into account fundamental information, they are forced to withdraw liquidity during periods of market stress to avoid being adversely selected.

Despite this disadvantage under stress conditions, their informational advantage over human trades under normal conditions has allowed them to grow to become the dominant liquidity providers in all of the largest, most liquid markets.

Some more details:

Adverse selection is the enemy of liquidity supply. When shocks of unknown origin cause sudden price declines, HFTs may have reason to assume that the shock is being driven by fundamental news (e.g., if the price decline follows a complex macro surprise or dramatic policy announcement). Under these circumstances, HFTs are at higher risk of being adversely selected by more fundamentally informed traders, so their optimal response is to withdraw liquidity by widening their quotes or by withdrawing them altogether. As selling continues, a feedback loop can arise where the resulting lack of liquidity causes bigger price declines, which then causes HFTs to supply even less liquidity, in some case even switching to strategies that aggressively demand liquidity rather than supplying it.

The big problem is what happens when the “market”, which in the past 9 years has been centrally-planned by central banks and hardly if ever “allowed” to drop, is pushed into a mode of forced price discovery and where HFTs no longer provide the much needed liquidity. That is when we will see just how broken and fragile the quote-unquote market has become. It is also when we believe we will see the first marketwide, and indefinite halt of all trading.

The research of Raman et al. and many others suggests that “flash crashes” may reflect such feedback loops. On the historical evidence thus far, the rising incidence of “flash crashes” (including the VIX spike) appears to represent no more than a modest (if occasionally expensive) source of execution risk. We worry this may simply be good luck—the fundamental backdrop has been relatively benign. Under different circumstances, namely scenarios where markets are trying to absorb complex headlines that may indicate a major decline in the fundamental outlook, we worry that such market conditions could discourage the supply of algorithmic liquidity for a more sustained period. Even if this period were to last just one day, that might be enough to fuel a crash on the order of “Black Monday” (October 19, 1987), when the Dow Jones fell over 22% in one day. Such a crash would give buy-side investors time enough to (falsely) infer from falling prices that there had been a shift in market sentiment, in which case a flash crash “bounce” might fail to materialize. Feedback loops between price declines and funding liquidity might further complicate the market’s ability to bounce back.

It gets worse, because all that bad stuff you’ve read about HFT on this website over the years, well guess what? It was correct. And here is Goldman with the validation:

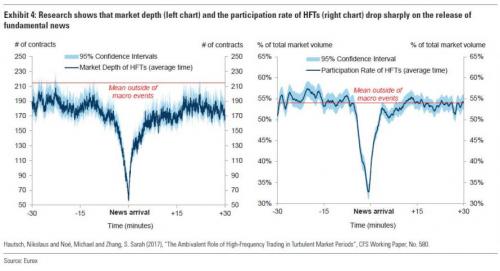

Indeed, even more to the point, a recent report on the behavior of HFTs in the Eurex Bund Futures market around high-impact macroeconomic news announcements suggests precisely this—that HFTs systematically withdraw liquidity when “complex” (non-routine) information is known to be in the market. Exhibit 4 is borrowed from this report and shows how HFTs behave during the 60-minute interval around major news events. The left chart shows that the overall depth in the market declines sharply around the announcement time (around 70% on average). The right chart displays the participation rate by HFTs, which declines from around 50% 10 minutes before the announcement to 33% at the time of release. This is also a drop of around 70%, suggesting that the drop in market depth is due mainly to the retreat of HFTs.

This HFT reluctance to supply liquidity shown in Exhibit 4 arguably shows the logic of adverse selection at work. When complex fundamental information enters the market, human traders gain the information advantage, and HFTs pull back. This insight cautions against taking comfort from the benign history of flash crashes thus far.Exhibit 4 also shows that, once the fundamental uncertainty clears, HFTs quickly resume supplying liquidity. We worry, however, about a future scenario where the fundamental uncertainty does not immediately clear. These scenarios would not necessarily be standard macro announcements, but rather complex “news shocks” (like unconventional monetary actions) which are not easily quantified by algorithms.

In this world of adverse selection – which as we predicted in April 2009 is due to the pervasive influence of HFTs, quants and central banks, Goldman unveils the most dramatic warning about just how broken the market has become:

“as machines have replaced people, and speed has replaced capital, the ability of the market’s liquidity providers to process complex information may lead to surprisingly large drops in liquidity when the next crisis hits.“

Which brings us to Goldman’s conclusion, one which can have been taken from any one of our hundreds of articles explaining how HFTs, and central banks, have broken the market, and it begins as follows: “Future flash crashes may not end well.”

While we focus on one particular theory for why “trading fragility” may be rising (namely, adverse selection), we see other risks that are in some sense more obvious. For example, the substitution of speed for capital means that ever larger amounts of trading volume are backed by too-thin capital cushions; liquidity supply could collapse on a large operational loss. Alternatively, if a flash crash were to occur against a more negative macro backdrop, it could inadvertently reinforce the market’s interpretation of “bad news.” Given the rapid evolution of the market, there are many other possible reasons to worry about a rise in trading fragility, not least of which are the “unknown unknowns.”

And here is Himmelberg with what he thinks are the implications for investors:

We see at least two potential implications for investors. First, investors should not be lulled into a false sense of complacency by the degree of macroeconomic stability that has characterized this recovery. As we have previously argued, this “Greater Moderation” in the volatility of growth and core inflation potentially—hence the general feeling that we are on a slower but more predictable growth path—may partly explain why our estimates of the risk premia for bonds and equities have fallen to such low levels in this expansion. But this may overlook the risk that “markets themselves” are a rising source of risk.

Second, the quality of trading liquidity for even the biggest, most heavily-traded markets should not be taken for granted. Tails may be fat, so investors should carefully consider the “vol of vol” when hedging their market risk.

Translation: run for the hills, because while Goldman may have finally grasped what we have said all along about how broken the market is at the micro level, the next “revelation” will be how HFTs have worked in concert with central banks to create the world’s most broken capital markets. And the punchline: central banks are now starting to withdraw liquidity, and while still positive for a few more months, starting some time in mid-2018, the central bank net liquidity injection will turn negative for the first time since the crisis.

At that moment, when the market has a sudden, collective “ligthbulb” moment and realizes that the only source of equity upside is now actively deleveraging risk assets, the selling will begin – selling which will be joined by HFTs – but by then it will be too late to sell.

* * *

Finally, for readers who want to read more on just how broken the market truly is, here are some of the most notable warnings from the likes of Bank of America’s Benjamin Bowler…

… who explicitly noted the market’s increasing fragility on numerous occasions…

… and how the Fed rushed to bail it out on every single occasion…

… as well as Fasanara Capital…

… and Artemis Capital, which too has been warning about the market’s growing instability for years.

* * *

We will leave with what we said back in April 2009, as nothing has changed since then:

“what happens in a world where the very core of the capital markets system is gradually deleveraging to a point where maintaining a liquid and orderly market becomes impossible: large swings on low volume, massive bid-offer spreads, huge trading costs, inability to clear and numerous failed trades….

the consequences will likely be unprecedented, with dramatic dislocations leading the market both higher and lower on record volatility. Furthermore, high convexity names such as double and triple negative ETFs, which are massively disbalanced with regard to underlying values after recent trading patterns.“

February 5 was just the preview of the main event.